Protect Retirement Accounts Bankruptcy

Can Bankruptcy Protect My Retirement Accounts and 401(k)?

protect-retirement-accounts-bankruptcy-401k

Learn how bankruptcy may affect 401(k)s, IRAs, pensions, and retirement accounts in NY and NJ before using savings to pay debt.

ATTORNEY ADVERTISING

Can Bankruptcy Protect My Retirement Accounts and 401(k)?

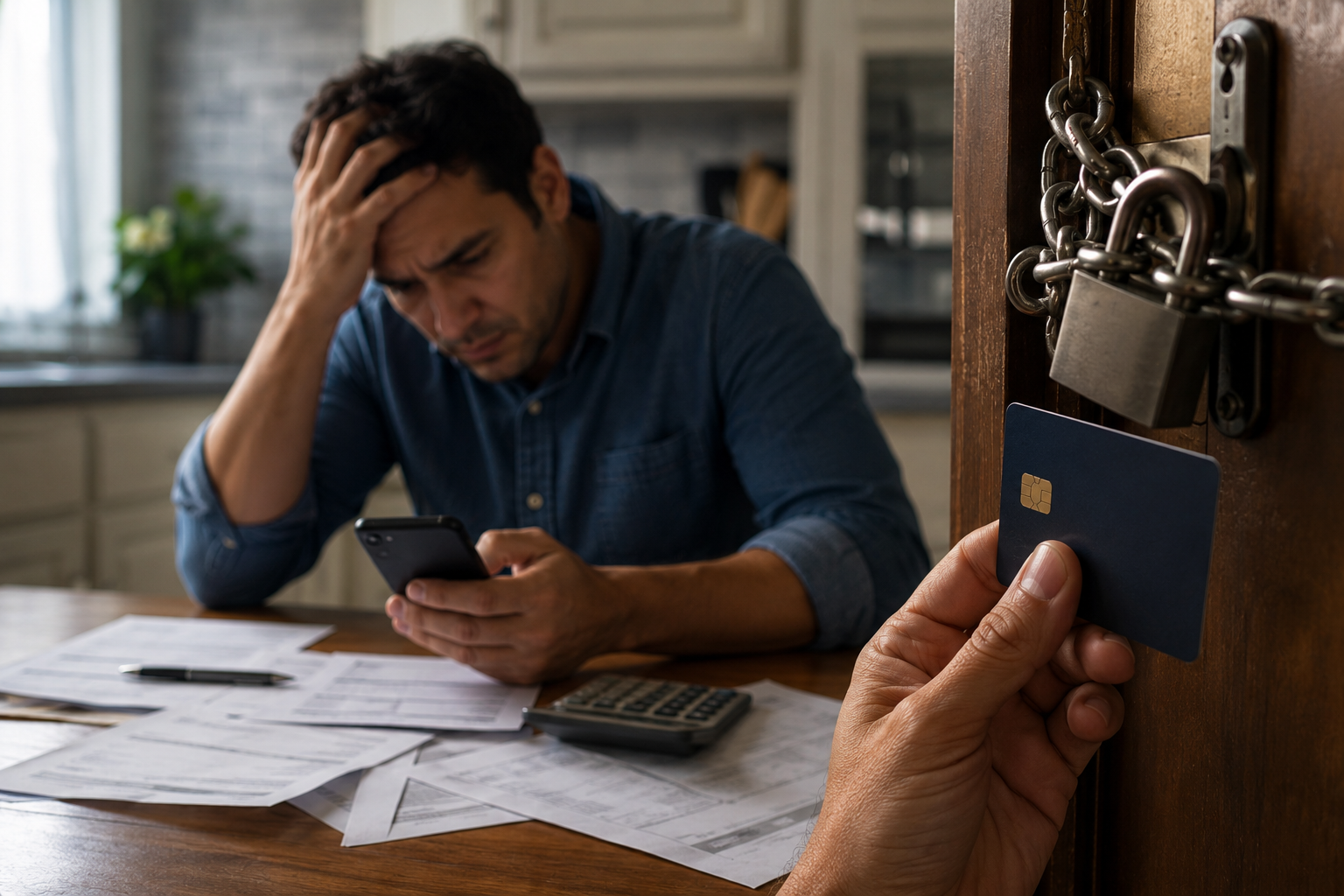

One of the biggest fears people have when considering bankruptcy is losing their retirement savings.

Many individuals spend years building a 401(k), IRA, pension, or other retirement account. As debt problems become more serious, some people delay seeking help because they believe filing bankruptcy means losing everything they worked hard to save.

In reality, retirement accounts are often treated differently than other assets. Depending on the type of account and the circumstances involved, bankruptcy law may provide significant protections for retirement funds.

Understanding these protections may help individuals make informed decisions before taking actions that could unintentionally affect their long-term financial security.

Do People Lose Their Retirement Accounts in Bankruptcy?

One common misconception about bankruptcy is that filing automatically means losing retirement savings.

In many situations, certain retirement accounts receive special protection under federal bankruptcy law and other applicable exemption laws.

However, whether a particular account is protected depends on numerous factors, including:

- The type of retirement account

- The source of the funds

- Whether contributions were handled properly

- The chapter of bankruptcy being considered

- Applicable federal or state exemption laws

- The facts of the individual case

Because every case is different, individuals should consult a qualified bankruptcy attorney regarding their specific circumstances.

Which Retirement Accounts May Receive Protection?

Examples of retirement assets that may receive protection under certain circumstances include:

- 401(k) accounts

- Traditional IRAs

- Roth IRAs

- Pension plans

- Profit-sharing plans

- SEP IRAs

- SIMPLE IRAs

- Certain government retirement plans

The extent of any protection depends on federal law, applicable exemptions, and the facts of each case.

Should You Cash Out Your 401(k) Before Filing Bankruptcy?

Many people consider withdrawing retirement funds to pay credit cards, personal loans, medical bills, or collection accounts.

Unfortunately, some individuals discover later that using retirement savings to pay unsecured debts did not solve the underlying financial problem.

In certain situations, using retirement funds before exploring all available options may create tax consequences, early withdrawal penalties, and permanent loss of retirement savings.

Before making decisions involving retirement accounts, individuals should consult legal and financial professionals regarding their circumstances.

Can Creditors Take My 401(k)?

Outside bankruptcy, retirement accounts often receive important protections under federal law.

Whether creditors may access retirement funds depends on many factors, including:

- The type of creditor

- Whether a judgment exists

- The type of retirement account involved

- Applicable federal and state laws

- Any exceptions or limitations that may apply

Because retirement protection rules can be complex, individuals should obtain advice before assuming an account is fully protected or fully exposed.

Can Bankruptcy Help Protect Retirement Savings?

In some situations, bankruptcy may help individuals address debt while preserving assets that receive protection under applicable law.

Whether bankruptcy is appropriate depends on numerous factors, including:

- Total debt

- Income

- Existing lawsuits

- Available exemptions

- The type of assets involved

- Long-term financial goals

Bankruptcy is one possible option among several, and every financial situation requires individual analysis.

Common Mistakes People Make With Retirement Accounts and Debt

Some individuals unknowingly place retirement savings at risk by making financial decisions before seeking guidance.

Common mistakes may include:

- Cashing out a 401(k) to pay credit cards

- Borrowing from retirement funds without understanding the consequences

- Waiting too long before exploring options

- Using retirement money to keep up with minimum payments

- Assuming bankruptcy means losing everything

- Failing to review available exemptions before taking action

Understanding available options before taking irreversible actions may help preserve long-term financial stability.

Is Bankruptcy the Only Option?

Not necessarily.

Depending on the circumstances, some individuals may explore alternatives such as debt negotiation, payment arrangements, debt consolidation, financial planning, or bankruptcy.

Not all options may be available or suitable for every person. Pagán López Law provides legal representation in consumer bankruptcy matters. Individuals considering debt consolidation, financial planning, or other non-bankruptcy solutions may wish to consult financial professionals, credit counselors, or other appropriate advisors regarding those alternatives.

Determining the best strategy requires an evaluation of each individual’s financial circumstances.

Frequently Asked Questions

Can bankruptcy take my 401(k)?

Under federal bankruptcy law, 401(k) accounts and many ERISA-qualified retirement plans are generally protected from creditors in bankruptcy. Certain IRAs may also receive protection subject to applicable limits and exemptions. However, protection depends on the type of account, the source of funds, and the facts of each case.

Can I lose my IRA if I file bankruptcy?

Certain IRA accounts may receive protection under applicable bankruptcy exemption laws. However, IRA protection may be subject to limits and depends on the type of IRA, account history, source of funds, and applicable law.

Should I use my retirement money to pay credit cards?

Using retirement funds to pay unsecured debt may create tax consequences, penalties, and long-term financial harm. Before withdrawing retirement funds, individuals should consult qualified legal and financial professionals regarding their specific situation.

Are pensions protected in bankruptcy?

Certain pension plans and retirement benefits may receive protection depending on applicable law, the nature of the plan, and the facts of the case.

Is bankruptcy better than cashing out a 401(k)?

Every financial situation is unique. Bankruptcy is one option among several and requires individual evaluation. A bankruptcy attorney can explain how bankruptcy may affect protected retirement assets, while a financial professional can address investment and tax considerations.

Final Thoughts

Many people delay seeking legal advice because they fear losing their retirement savings.

However, retirement accounts often receive protections that surprise individuals who are struggling with debt.

Before liquidating retirement assets or making major financial decisions, understanding how bankruptcy law may affect those assets can help individuals protect both their present and their future.

Pagán López Law – Office HQ

96-04 Northern Boulevard, Corona NY, 11368

Phone: (646) 216-8881

WhatsApp: (347) 434-3041

Email: info@paganlopezlaw.com

Attorney Advertising

This post is for informational purposes only and does not constitute legal advice. Outcomes vary by case. Consult a qualified bankruptcy attorney before taking action. Reading this post or contacting the firm does not create an attorney-client relationship.